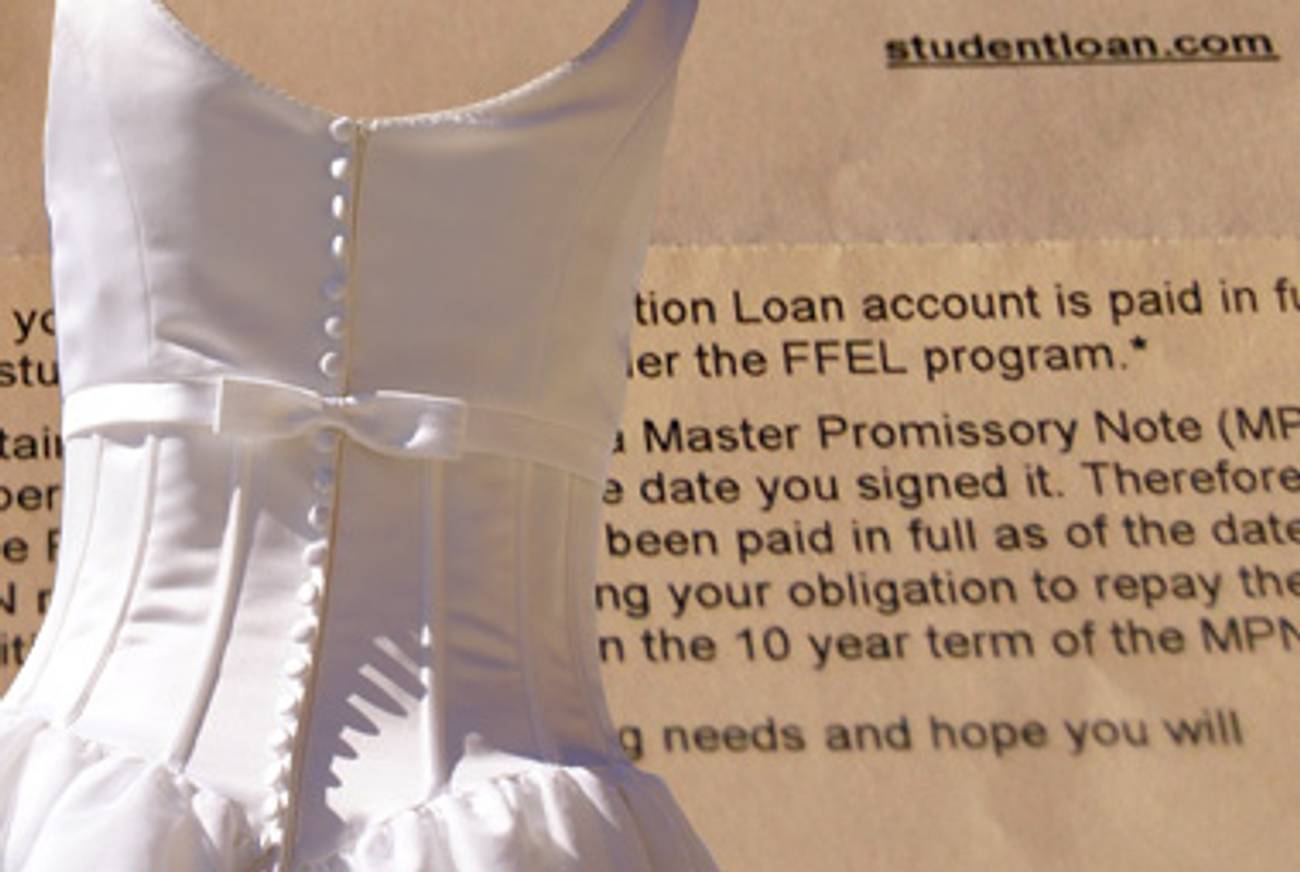

As a 27-year-old, marginally employed freelance writer and part-time Hebrew school teacher, my income fluctuates wildly from month to month. After I send in my rent check and pay for food and other basics, there is often little left over. A few years ago, I was faced with a rather stark choice—pay my medical-insurance premiums or my monthly student loan bill, money that I had borrowed to pay for an MFA in creative writing, which I completed in the spring of 2008. (If you’re questioning the wisdom of pursuing a Master’s degree in something as woolly as writing, get in line behind me.) I went with my health over my debt and deferred the loans. But I wasn’t comfortable deferring them indefinitely. The interest was steadily accruing, and I was panicking.

I had been raised to fear debt. My mother had made the mistake of cosigning credit card applications with my father when they were married. They divorced when I was 8, he left Brooklyn for Florida, and my mother got stuck with his bills when he was unable to pay them. My mother, a New York City public school teacher, raised me and my sister alone. Throughout my elementary-school years, our dinners were constantly interrupted by calls from my father’s creditors. Now I almost always pay off my monthly credit-card balances in full and carefully budget for all expenditures. Yet no amount of frugality could decrease the amount I owned to the educational-loan company. As the end of my most recent renewal approached, there was only one place I knew I could turn—my nuptial fund.

By all rights, this money should have already been spent. In the Orthodox community where I grew up, girls my age are married, in which case they are called women. I recently attended my 10-year high-school reunion, and I could count the number of singles on one hand. (And a few of the unattached were divorcees.) The rest of my former classmates had already begun constructing a bayis ne’eman b’Yisroel, a faithful home in Israel, as we had been taught to do in our all-girls yeshiva. I still lived in a studio apartment.

So, the money my mother had set aside for my wedding was still there. That she was able to squirrel away a small yet significant sum of money to pay for the hoped-for ceremony and party on her public servant’s salary and eventually, pension, was impressive and a sign of how much my marrying mattered to her.

I only knew about the money because my mother, in the tradition of older folk, likes to speak about her will. She turned 70 in August, but she has been engaged in this sort of talk since I was in grade school. When I was little and used to light the Sabbath candles with her on Friday night, she’d point to the two brass candlesticks and say, “These will be yours in 120 years.” (Since Moses died at the age of 120, many traditional Jews believe that he set a life-span precedent and people cannot live beyond this age.)

The first time she brought up the wedding money, I was 15, and we were in the car driving to school. “I need to speak to Shloimie,” she said. Shloimie is her nephew and a lawyer and is therefore the family repository of legal advice. “I need to add a clause to my will so there will be money so you can have a wedding as nice as Lisa’s.” My older sister, nearly eight years my senior, had just gotten married, and the affair, while hardly posh, was attended by 200 friends and family.

“Uh-huh,” I answered nonchalantly as I stared out the window. I didn’t like what she was implying—that she wouldn’t be around for my wedding as she had been for my sister’s.

Since then, my mother has brought up the wedding clause many times. I usually brush off her mention of final arrangements by saying, “You’ll be annoying the crap out of me for many years to come.” This makes her chuckle.

Yet knowledge of it is burrowed deep in my mind. I’ve often wondered: How much money had she set aside? Could I ask for some of it?

This past summer, I couldn’t stop thinking about the fund. Why did I have to wait until I got married? What if I never got married? If the point of this money was to increase my happiness by giving me the wedding of my dreams—well, I had other ideas about what would make me happy. I kept repeating these arguments to myself until I almost believed them.

The truth was that I didn’t actually want to give up my wedding. Although I’ve never been the type to fantasize about a dress or flower arrangements, I always thought I’d have a wedding. And I thought it would’ve happened by now. Even as I dropped the trappings of Orthodox observance, I didn’t completely let go of getting married altogether.

I entered my late 20s still single and without a significant relationship under my belt. I might never get married, I realized, and there is nothing I can do about it. My career, on the other hand, is something I can make happen. Even in today’s dismal media marketplace, I can network, hustle, and work several jobs into the wee hours of the morning. But I couldn’t force the universe to introduce me to the right man, and I couldn’t force that man to tolerate me. When I thought about where the money would have the greatest impact on my life, I decided that funding my education and career was a sounder bet than a wedding that might never take place.

Last summer, I asked my mother to meet me in my neighborhood. After my mother parked her car in front of my building, we walked to a local café. It was a muggy August day; I was going slow, but my mother was moving even slower. I realized, as I had been realizing many times over the last few years just how old my mother was getting. If at 15, I nonchalantly believed my mother would be at my wedding, I wasn’t as confident at 27.

At a popular hipster hangout we settled into the lumpy couch with our coffees and desserts. I sat silently for a few minutes, staring at artwork on the walls. I was suddenly nervous. I hadn’t planned how to broach the subject. There hadn’t seemed a point to rehearsing.

Finally, I simply asked. It’s hard for me to remember my exact words, but I muttered something about money and a wedding, and said, “I’d like to pay off my school debt.”

Her face fell. “You’re not going to get married?” she asked me, her lower lip quivering.

I tried to reassure her, even though I too was uncertain. I looked down at my dry scone, wondering why I had even bothered ordering it.

I tried to remember all the reasons I had decided to bring this up. I began speaking: It was a good financial decision for her, I said. Costs are only going up. It’s better to pay for a “wedding” in 2010 than in 2012 or 2015. Also, my mother has always been supportive of my career goals. She understood that by alleviating some of the financial burdens caused by my education debt, I could spend more time writing. And finally as a woman who married late herself—at 31, which was and still is ancient in the Orthodox Jewish community—only to get divorced 18 years later, I think she recognized that the wedding is, in the end, just a party. It can make you happy for just one night whereas student loans can make you unhappy for decades. (In that respect, education debt is like a bad marriage.)

As I finished stating my case, she nodded slowly. I wasn’t sure if she agreed with my points or was acquiescing to my request. She gradually conceded that a big, fancy wedding didn’t fit my personality profile. “I always saw you getting married barefoot on a beach somewhere anyway,” she said, brightening up.

We entered final negotiations in the café. The number we settled on was based on the amount she paid for my sister, nearly eight years my senior, to get married, adjusted for inflation since she wed in 1998. I was insistent on this point since I had been fooled as a child when the discussion was about my mother’s contribution to my college tuition. “I will pay just as much for you to go to college as I did for your sister,” she had said. This seemed perfectly fair and generous to a 7th grader. It wasn’t until I was a senior in high school that I realized that I got the raw end of the deal. “But tuitions are much higher now than when Lisa was in college,” I told my mother.

“That was our deal,” she would remind me, shaking her head.

Despite my shrewdness this time around, my mother still low-balled me. “I’m keeping a few thousand dollars,” she said, writing a figure on the napkin. “Because when you do get married, I still want to throw you a small party.”

I almost objected to this change but then thought better of it. She didn’t owe me the money. She finished raising me a long time ago, and all of it was a gift. I kissed my mother on the cheek. I liked that she was still planning my wedding, that she was holding out hope that I will eventually find love with a kind and supportive man, even if I don’t believe it will happen for me. Her faith restored a little of my own. As I walked home, I envisioned professional success, a steadier income, and monetary solubility. Maybe, I thought, I will get to use some of this money for my own wedding. Maybe.